Every year, trillions of dollars move between businesses across borders, and yet the actual experience of sending or receiving an international B2B payment still feels stuck in the past. Wire transfers take days. Invoices get lost between currencies. Reconciliation eats up hours that finance teams don't have. If you're running a distribution company or a mid-market procurement operation, you've probably felt this friction firsthand: a supplier in Germany quotes in euros, your customer in the Philippines pays in pesos, and your accounting system only speaks dollars. The global B2B cross-border payments market was valued at $31.7 trillion in 2024, and it's still growing fast. Yet the infrastructure supporting most of these transactions hasn't kept pace with the volume. This guide is built for founders and finance leaders at companies doing $1M to $50M in revenue who need practical, hard-won lessons on how to move money internationally without bleeding cash on fees, delays, and manual processes. We'll walk through the full lifecycle, from quoting to settlement, and show you where the real opportunities for speed and savings live.

The Evolution of Global B2B Trade and Payment Systems

International trade isn't new. What's new is the speed at which mid-market companies are expected to operate across borders. A construction distributor in Texas sourcing steel from South Korea, a SaaS reseller in London invoicing clients in Brazil: these aren't edge cases anymore. They're Tuesday.

The payment infrastructure supporting these transactions, though, was largely designed for large enterprises with dedicated treasury teams. Correspondent banking networks, SWIFT messaging, and multi-day settlement windows were built in an era when a five-day payment cycle was considered acceptable. For an SME doing $5M in annual revenue with thin margins, five days of float on a $200,000 wire transfer isn't just inconvenient. It's a cash flow crisis.

The shift toward digital payment rails, real-time settlement networks, and API-driven platforms has started to close this gap. But adoption remains uneven. Many businesses still rely on a patchwork of bank portals, email-based invoice approvals, and manual FX conversions that introduce errors and delays at every step.

Current Challenges in Cross-Border Invoicing and Collections

The pain points are specific and measurable. First, there's the FX problem: most SMEs don't have access to interbank exchange rates. They're paying a markup of 1% to 3% on every conversion, which on a $10M annual spend means $100K to $300K lost to hidden fees alone. Second, invoice reconciliation across currencies is a nightmare. When a buyer pays $49,800 on a $50,000 invoice because their bank deducted intermediary fees, someone on your team has to chase the shortfall.

Collection timelines stretch even further when you add time zone differences, language barriers, and varying payment customs. Net-30 terms in the US might functionally become net-60 or net-75 when you're collecting from a buyer in Southeast Asia who processes payments on a different cycle. One client we worked with, a building materials distributor, discovered they were carrying an average of 47 days of receivables on international orders versus 29 days domestically: a gap that was quietly strangling their working capital.

Why Traditional Banking Fails SMEs and Mid-Market Companies

Banks are excellent at moving large sums for large clients. They're not designed to serve the needs of a $15M distributor who sends 200 international invoices per month across eight currencies. The fee structures alone tell the story: $25 to $50 per outgoing wire, $15 to $25 per incoming wire, plus FX spreads, plus intermediary bank charges that are often invisible until the payment arrives short.

Beyond fees, the reporting is fragmented. Most banks provide transaction-level data that doesn't map cleanly to your ERP or accounting system. You end up with a finance team spending hours each week manually matching payments to invoices, converting currencies in spreadsheets, and chasing discrepancies. If you're a company hitting 30 to 50 international orders per month, this manual work becomes a breaking point. The cost isn't just in labor: it's in the decisions you can't make because your cash position is always two days behind reality.

The Quote-to-Payment Lifecycle for International Transactions

Most businesses think of payments as the last step in a transaction. That's the wrong mental model, especially for cross-border deals. The payment experience actually begins the moment you generate a quote, because that's when you lock in pricing, currency, and terms that will ripple through procurement, fulfillment, and collection.

Treating the quote as a disconnected document, a PDF emailed to a prospect, means you're creating a manual handoff at the very start of the transaction. Every handoff is a chance for errors, delays, and lost context. The companies that move fastest internationally are the ones who treat the entire quote-to-payment chain as a single, connected workflow.

Starting at the Source: Treating the Quote as a Live Transaction State

Here's a founder-to-founder insight that took us years to learn: the quote is the transaction. It's not a precursor. It's not a marketing document. It contains the pricing, the line items, the currency, the payment terms, and the delivery expectations that will govern everything downstream. When you treat it as a static PDF, you're forcing your team to re-enter that data into a purchase order, then again into an invoice, then again into your payment system.

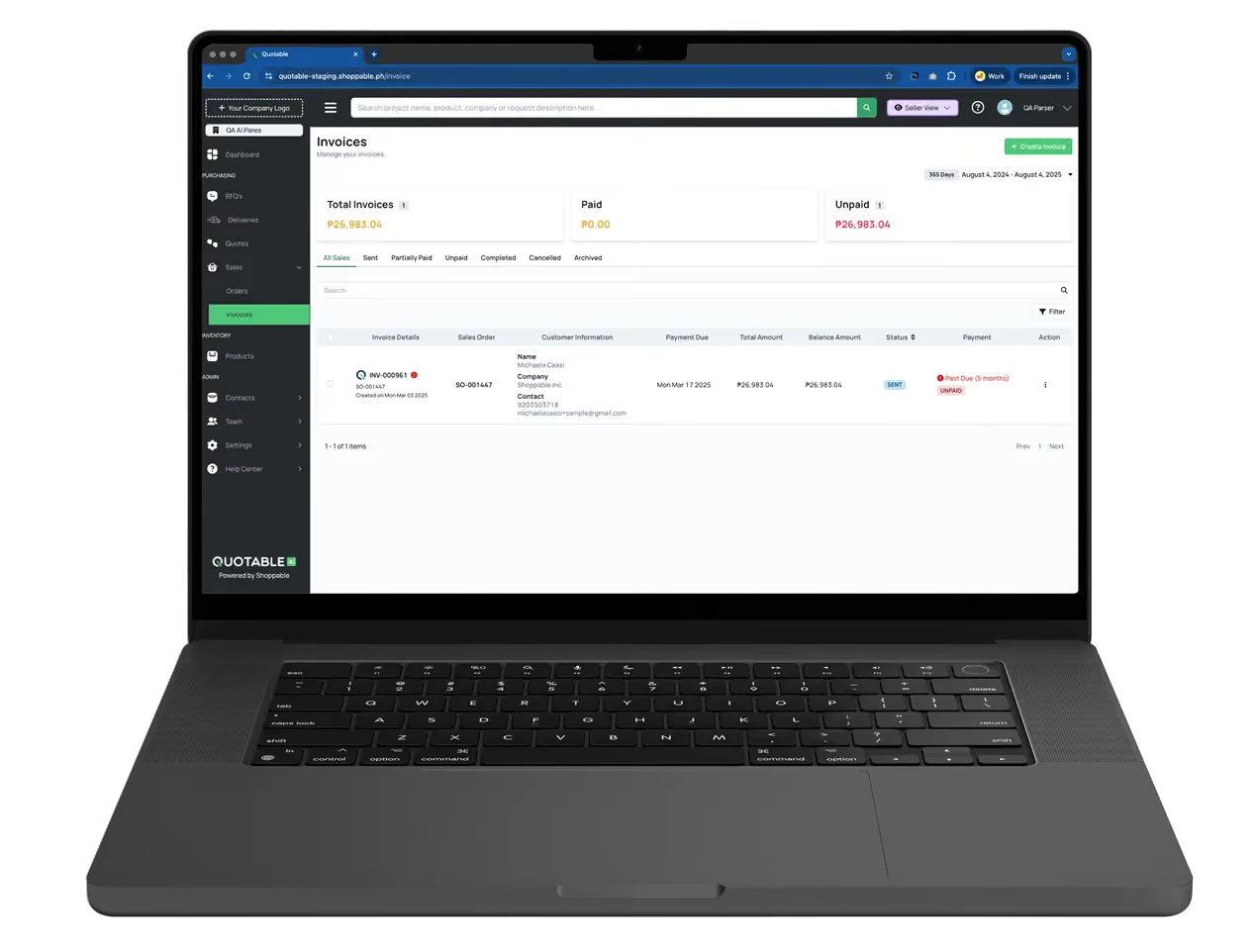

This is where platforms like Quotable AI take a fundamentally different approach. Instead of treating the quote as a document, it's treated as a live transaction state that flows directly into procurement, invoicing, and payment without manual re-keying. The quote carries its data forward. If a buyer in Munich approves a quote denominated in euros, that currency, those line items, and those terms automatically populate the invoice and payment request. No one has to re-enter anything.

For a company processing 100 quotes per month across multiple currencies, this isn't a nice-to-have. It's the difference between a two-person finance team that's drowning and one that's actually managing cash flow proactively.

Integrating Procurement and Fulfillment into the Payment Workflow

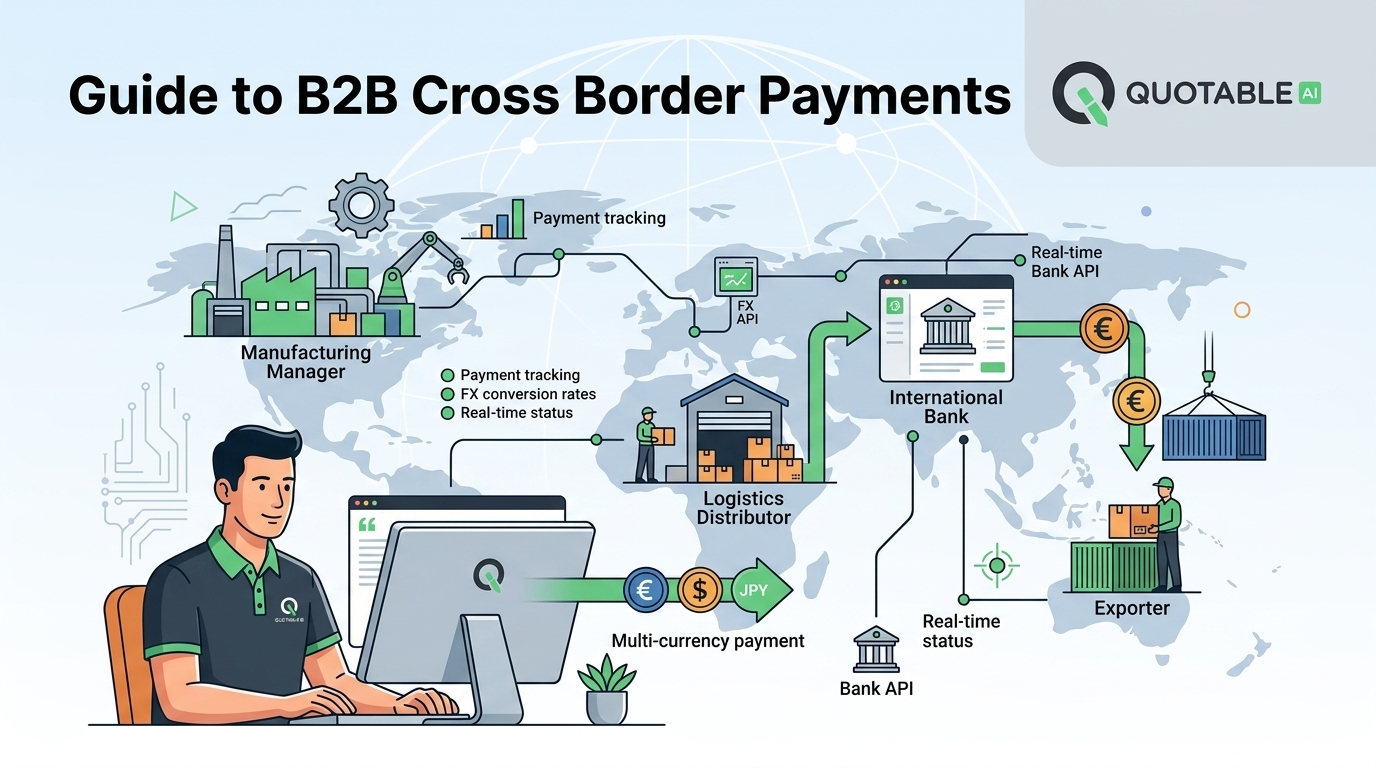

Cross-border transactions don't just involve a buyer and a seller. They involve freight forwarders, customs brokers, banks, and sometimes multiple suppliers fulfilling a single order. When your payment workflow is disconnected from procurement and fulfillment, you lose visibility into landed costs: the true cost of goods once you factor in duties, freight, insurance, and FX impact.

Consider a mid-market construction company importing prefabricated panels from a supplier in Turkey. The quoted price is $85 per unit. But by the time you add ocean freight, customs duties, insurance, and a 2% FX markup from the bank, the landed cost is $104 per unit. If your payment system doesn't track these components, you're making margin decisions based on incomplete data.

The fix is connecting your procurement documents, bills of lading, packing lists, and customs declarations, directly to your payment and invoicing workflow. When a shipment clears customs, the system should automatically reconcile the landed cost against the original quote and flag any variance. This kind of three-way match between the quote, the purchase order, and the actual payment is standard practice in enterprise procurement. It's increasingly accessible to mid-market companies through integrated platforms.

Optimizing Global Cash Flow with Data Orchestration

Cash flow management for international businesses isn't just about getting paid faster. It's about having accurate, real-time visibility into what you're owed, what you owe, and where your money is at any given moment. Data orchestration, the practice of connecting disparate data sources into a single coherent view, is what makes this possible.

Most SMEs are running their international operations across three to five disconnected systems: a CRM for quotes, an ERP for orders, a banking portal for payments, an email inbox for approvals, and a spreadsheet for FX tracking. Each system holds a piece of the truth, but none holds all of it. The result is that your CFO is making decisions based on data that's at least 24 to 48 hours stale.

Automating Sales Quotations and Multi-Currency Invoicing

The single highest-ROI automation for most B2B companies doing cross-border business is connecting their quoting and invoicing systems. When a sales rep generates a quote in British pounds and the buyer approves it, the invoice should generate automatically in the same currency with the correct payment methods, bank details, and regulatory information already populated.

Quotable AI's universal AI parser handles this by automatically extracting and structuring data from business documents: quotes, invoices, purchase orders, and bills of materials. This means you don't need to manually encode each document. The system reads the quote, understands the line items, currency, and terms, and carries that data forward into every downstream document.

For multi-currency operations, this also means your system should be calculating FX exposure in real time. If you've quoted $500,000 in euros across 15 open proposals, you should know your euro exposure at any moment, not discover it at month-end close. Companies that automate this process typically reduce invoice processing costs by 60% to 80%, and more importantly, they eliminate the reconciliation headaches that plague manual workflows.

Reducing Transaction Latency in Construction and Manufacturing

Construction and manufacturing companies face a unique challenge: their payment cycles are tied to physical milestones. A steel fabricator doesn't get paid when the invoice is sent. They get paid when the material is delivered, inspected, and approved. This creates long payment cycles that are compounded by cross-border delays.

If you're a manufacturer in Monterrey shipping to a general contractor in Phoenix, your payment timeline might look like this: 5 days for shipping, 3 days for inspection, 10 days for internal approval, and then net-30 payment terms. That's 48 days from shipment to cash. Add a 3-day wire transfer processing time and you're looking at 51 days.

Reducing this latency requires two things: faster approval workflows and faster payment settlement. On the approval side, systems that allow buyers to approve and pay through no-login links, without needing to create accounts or learn new software, dramatically reduce the friction. On the settlement side, offering multiple payment methods (bank wire, ACH, credit cards, and e-wallets) lets buyers choose the fastest option available to them. A buyer who would take 30 days to process a wire transfer might pay in 3 days via credit card if you give them the option.

Compliance and Security in Cross-Border Data Transfers

Moving money across borders means moving data across borders, and that triggers a complex web of regulatory requirements. GDPR in Europe, CCPA in California, PIPL in China: each jurisdiction has its own rules about how financial data can be stored, transferred, and processed. For a mid-market company without a dedicated compliance team, this can feel overwhelming.

The key compliance areas for B2B international payments break down into three categories:

- Know Your Customer (KYC) and Anti-Money Laundering (AML): you need to verify the identity of your trading partners and monitor transactions for suspicious patterns. This isn't optional. Penalties for AML violations can reach millions of dollars even for mid-sized companies.

- Sanctions screening: every cross-border payment should be screened against OFAC, EU, and UN sanctions lists. Sending a payment to a sanctioned entity, even unknowingly, can result in severe penalties and criminal liability.

- Data residency and transfer requirements: some jurisdictions require that financial data about their citizens or businesses be stored within their borders. If you're invoicing a client in Brazil, you may need to comply with LGPD requirements about how that invoice data is handled.

The practical solution for most mid-market companies is to use a payment platform that handles compliance as a built-in function rather than an add-on. Your system should automatically screen transactions, maintain audit trails, and flag potential issues before they become legal problems. This is one area where trying to DIY a solution from spreadsheets and manual checks isn't just inefficient: it's genuinely risky. SOX compliance requirements, for companies that fall under them, add another layer of documentation and control requirements that manual processes simply can't satisfy reliably.

Data security is equally critical. Cross-border payment data is a high-value target for fraud. End-to-end encryption, role-based access controls, and real-time fraud monitoring should be non-negotiable features of any platform you use. If your current process involves emailing bank details in plain text, which is still shockingly common, you're one phishing attack away from a six-figure loss.

Future-Proofing Your Business with AI-Powered Payment Platforms

The next five years will see more change in B2B payment infrastructure than the previous twenty. Real-time payment networks are expanding globally. AI-driven document processing is eliminating manual data entry. And integrated platforms are collapsing what used to be five separate systems into one.

For mid-market companies, the strategic question isn't whether to modernize your cross-border payment operations. It's how to do it without ripping out your existing ERP and accounting systems. The smart money is on platforms that integrate with your current infrastructure rather than replacing it, adding an orchestration layer on top of your existing tools.

Scaling SME Operations from $1M to $30M Revenue

The operational requirements of a $1M company and a $30M company are fundamentally different, but the transition between them often happens faster than the infrastructure can keep up. A distributor doing $1M in international sales can probably manage with manual invoicing and a single bank relationship. At $5M, the cracks start showing. At $15M, the manual processes that worked at $1M are actively costing you money and customers.

The red flags that signal you've outgrown your current payment infrastructure are specific:

- Your finance team spends more than 10 hours per week on invoice reconciliation

- You've had at least two instances of duplicate payments or missed collections in the past quarter

- Your month-end close takes more than 5 business days because of international transaction reconciliation

- You can't tell your CFO your exact FX exposure on any given day

- Customers have complained about confusing payment instructions or delayed receipts

Right-sizing your solution means choosing a platform that handles your current volume while scaling to your target. Quotable AI, for example, connects with existing ERP and accounting systems so you don't have to abandon your current setup. You're adding a layer that automates the quoting, invoicing, and payment collection workflow while keeping your financial system of record intact. This approach lets you modernize incrementally rather than betting the company on a massive system migration.

Achieving 10X Faster Settlement via Integrated Operating Systems

The "10X faster" claim sounds like marketing, but the math actually works when you compare end-to-end cycle times. A traditional cross-border B2B transaction might follow this path: sales rep creates quote in Word (30 minutes), emails to buyer, buyer requests changes (2 days of back-and-forth), quote approved, order entered into ERP (20 minutes), invoice created manually (15 minutes), invoice emailed, buyer processes internally (10 to 15 days), payment initiated via wire (3 to 5 days for settlement). Total cycle: 15 to 22 days from quote approval to cash received.

An integrated system compresses this dramatically. Quote generated from a template with live pricing (3 minutes), buyer approves via a secure link (same day), invoice auto-generated from approved quote (instant), buyer pays through embedded payment options (1 to 3 days), settlement hits your account (same day to 2 days). Total cycle: 2 to 5 days. That's not 10X in every scenario, but for many mid-market companies, it's close.

The compounding effect matters even more than the per-transaction savings. If you're processing 200 international invoices per month and each one settles 10 days faster, that's a significant improvement in your cash conversion cycle. On $10M in annual international receivables, 10 fewer days of float is roughly $274,000 in freed working capital. That's real money you can reinvest in inventory, hiring, or growth.

Building Your Cross-Border Payment Strategy

The businesses that win in international B2B trade aren't the ones with the most complex systems. They're the ones that connect their quoting, procurement, invoicing, and payment workflows into a single, coherent process. Every manual handoff you eliminate is cash you recover and risk you remove.

Start by auditing your current cross-border payment cycle end-to-end. Measure the actual time from quote to cash, not the theoretical time. Identify where data is being re-entered, where approvals stall, and where FX costs are hiding. Then look for platforms that address your specific bottlenecks without requiring you to replace everything you've already built.

The opportunity is enormous. B2B cross-border payments are growing, and the companies that build efficient, automated payment operations now will have a structural advantage over competitors still emailing PDFs and chasing wire transfers. If you're ready to compress your quote-to-cash cycle and stop losing margin to manual processes, explore what an integrated platform like Quotable AI can do for your specific workflow. The best time to fix your payment infrastructure was two years ago. The second best time is now.